Inventory changes in accounting affect the fiscal year result (0)

Inventory changes in accounting means recording the correct value of inventory in the balance sheet, while the actual change in inventory is recorded in the income statement. The entry in the income statement directly affects the fiscal year’s result, whereas the entry in the balance sheet affects the company’s current assets.

Inventory Changes Affect the Fiscal Year Result

It’s clear that any accounting entry impacts the company’s result, and inventory changes are no exception. If inventory increases, the company’s profit—and consequently, the corporate income tax payable—also increases. Conversely, if inventory decreases, the profit and taxes payable decrease as well.

This is perhaps easiest to understand with an example: Suppose a company has purchased €10,000 worth of Moomin mugs for resale. At the time of purchase, the expense is recorded in the purchases account, reducing the fiscal year’s profit. However, at the end of the fiscal year, €5,000 worth of mugs remain unsold. This means that the unsold mugs are transferred from purchases to the balance sheet as current assets via an inventory change entry.

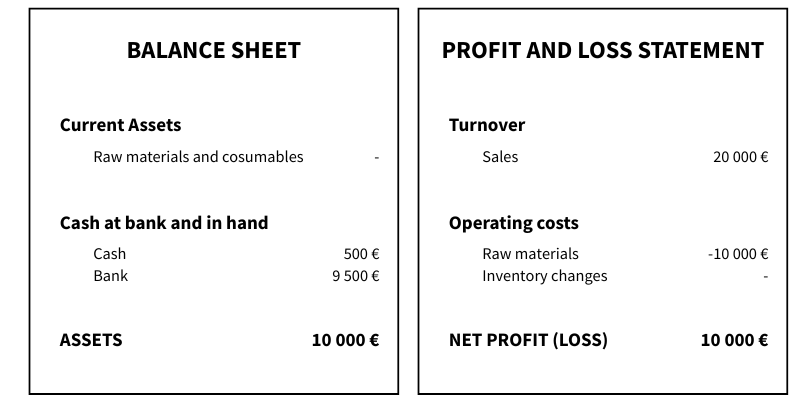

- If the company sells all the mugs, the income statement and balance sheet will look like this:

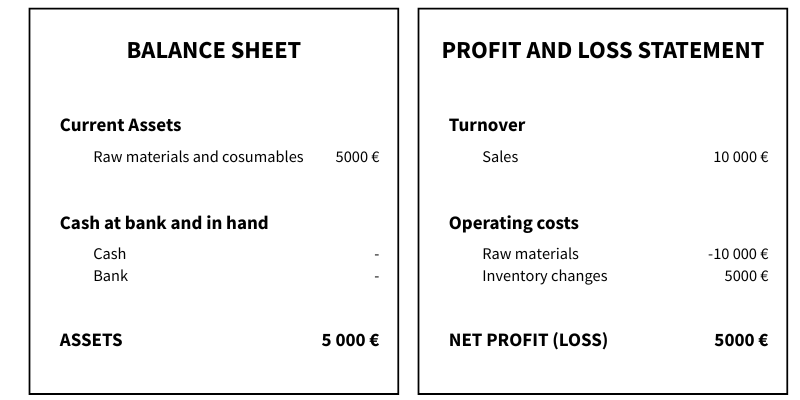

2. If the company sells only half of the mugs, the reports look like this:

Inventory Changes in Accounting

Now that we understand how inventory changes behave and how they affect the income statement and the balance sheet, let’s look at how to record an inventory change when there are already items in stock.

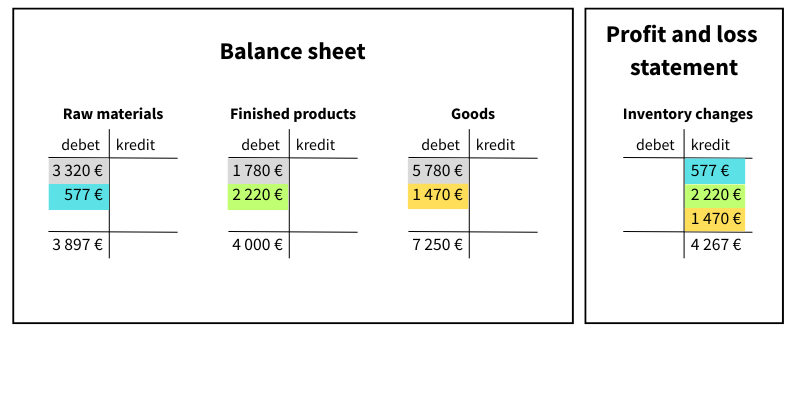

In Salli Singer’s previous financial statements, the total inventory value was €10,880, divided among balance sheet categories as follows:

– Raw materials and supplies: €3,320

– Finished products: €1,780

– Goods: €5,780

Now it’s time to prepare the new financial statements, and Salli has completed a stocktake and calculated the inventory value. The total inventory value is €15,147, divided among the balance sheet categories as follows:

– Raw materials and supplies: 3 897€

– Finished products: 4 000€

– Goods: 7 250€

The total inventory value has thus increased by €4,267. Each balance sheet category requires its own entry, which is done simply by calculating the change in each category and recording it as a debit in the balance sheet and a credit in the income statement.

In accounting, an inventory change is essentially just a reclassification of purchases from the income statement to the balance sheet. If the inventory value increases, a debit entry is made to the balance sheet and a credit entry to the income statement. Conversely, if the inventory value decreases, a credit entry is made to the balance sheet and a debit entry to the income statement.

Try right away!

A more advanced and easy accounting software SimplBooks with over 10,000 active users - register an account and you can try 30 days free of charge and risk-free (no financial obligations shall arise). Or try our demo version!

Leave a Reply