Dividends in accounting – how to record income and distributions? (0)

Dividends in accounting are recorded using the same principles as any other accounting entry. If a company receives dividends, they are considered income, and income increases on the credit side. If a company distributes dividends, they can be regarded as expenses, and expenses belong on the debit side.

In accounting, dividends are recorded in the financial year during which the underlying financial statements are approved and the decision to distribute dividends is made. In 2022, for example, dividends are distributed based on the 2021 financial statements, and once the general meeting has decided on the distribution, the dividends can be recorded for the year 2022.

Payment of dividends

It makes no difference whether dividends are paid to the entrepreneur personally or to someone else. In accounting, dividends behave exactly the same in both cases.

Receiving dividends in cash

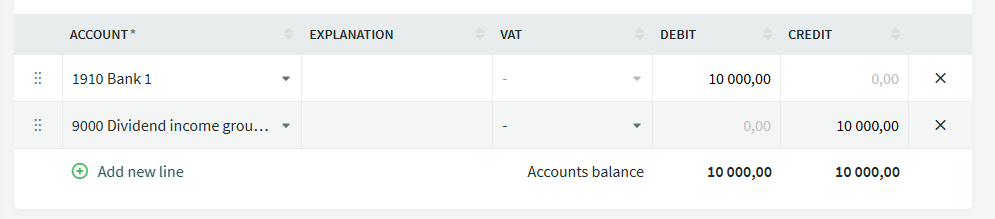

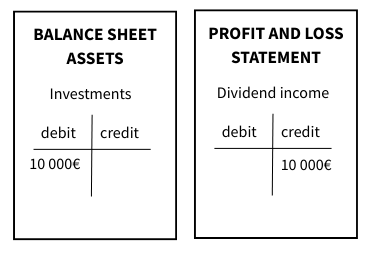

A company can receive dividends either in cash or in another form, such as shares or real estate. If the company receives dividend income in cash, dividends are treated like any other income. They are recorded as a debit to the bank account in the balance sheet, and a credit entry is made to dividend income in the profit and loss statement. In SimplBooks, the entry would look like this:

Receiving dividends in shares

Dividends can also be received in the form of shares. Their accounting treatment depends on whether the recipient engages in securities trading. If the company does not engage in securities trading, the shares are recorded under investments in fixed assets on the balance sheet and under dividend income in the profit and loss statement. If the company does engage in securities trading, the entry is slightly different and must be made in two parts.

The value of the shares is determined at the time the dividend becomes payable, and this fair value is used both for the dividend income entry and for recording the shares on the balance sheet. It is also important to remember that a company receiving shares as dividends is liable to pay transfer tax on those shares. The transfer tax paid forms part of the acquisition cost of the shares (i.e., the value at which the asset is recorded).

💡There have been changes to the treatment of transfer tax on share dividends as of 1 January 2025:

-

If a Finnish company distributes dividends in the form of shares, it is the distributing company that pays the transfer tax, and it is not taken into account in the taxation of the company receiving the dividend.

-

If a foreign company distributes dividends in the form of shares and pays the transfer tax, the transfer tax is considered dividend income for the receiving company. In this case, the recipient may choose whether to authorize the distributing company to file the transfer tax return or file it themselves.

Dividends in shares without securities trading

If a company receives shares as dividends and does not engage in securities trading, the shares are recorded under investments in fixed assets on the balance sheet and under dividend income in the profit and loss statement.

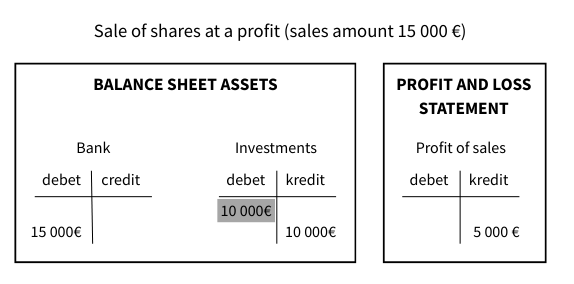

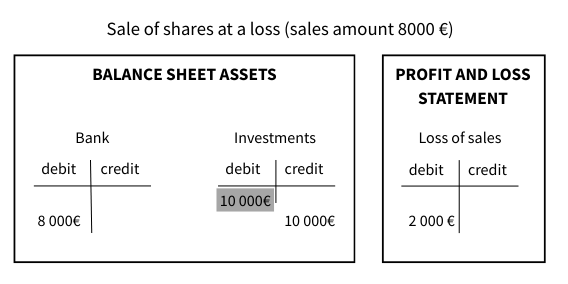

If the shares are later sold, the entry is a debit to the bank account and a credit to investments in fixed assets. In this way, the investments account is cleared with respect to those shares and they are no longer included in the accounting records.

However, shares are often sold at a different price than their acquisition cost, and depending on this, the sale will result in either a capital gain or a capital loss, which must be taken into account when recording the transaction.

Dividends in the form of shares and securities trading

If a company engages in securities trading and receives shares as dividends, the entry is slightly different. The shares will ultimately be recorded as inventory, but they cannot be posted there directly, because the corresponding account can only be an inventory change account. The entry therefore has to be made in two parts.

|

EXAMPLE First entry

Second entry:

💡So the final destination of the dividend income is inventory, but since it cannot be recorded there directly, it has to be routed through purchases and inventory changes. Inventory changes affect the amount of purchases by either increasing or decreasing it. In this case, the entries for purchases and inventory changes cancel each other out — meaning that the dividend entry does not affect the expense side of the income statement at all. |

|

EXAMPLE If the shares in the example are later sold, the sale must also be recorded in two parts. The proceeds from the sale are considered revenue for the company. First entry The entry is made at the selling price of the shares.

Second entry: The entry is made at the acquisition price of the share.

|

If a company engages in securities trading and sells its shares, no separate capital gain or loss arises, because the sale is always recorded directly as revenue.

Dividends in accounting are no more complicated than any other income or expense. Receiving dividends in the form of shares can be a bit confusing, whether the company engages in securities trading or not. However, it can be managed by taking the time to properly understand the subject. As a rule of thumb, income increases on the credit side and expenses on the debit side — and that principle will take you a long way, even in this matter!

Try right away!

A more advanced and easy accounting software SimplBooks with over 10,000 active users - register an account and you can try 30 days free of charge and risk-free (no financial obligations shall arise). Or try our demo version!

Leave a Reply