Liabilities – Long-term loans in accounting (0)

Debt capital is money invested in a company that does not belong to the company itself and must be repaid. In other words, it is someone else’s money – plain and simple, typically in the form of debt. Debt capital is divided into two categories: short-term and long-term. Short-term debt must be repaid within one year, while long-term debt has a repayment period extending beyond one year. So, if a loan or installment plan has a term longer than one year, it is considered long-term debt capital.

Long-term loan in accounting

Most often, a long-term loan in accounting refers to a bank loan or installment debt. It’s good to know that taking out a loan or repaying its principal does not affect the company’s profit for the financial year, as these entries appear only on the balance sheet. However, expenses and interest related to the loan repayment are recorded in the profit and loss statement, reducing the financial year’s result.

It’s best to create a separate account under the balance sheet’s long-term liabilities section for each loan. The account can be named using the loan number or another clear identifier. For example, if a company acquires a car through installments, the liability account could be named after the car’s make or license plate. Clear naming makes the balance sheet easier to read and helps match repayments to the correct loan – especially when the company has multiple loans or installment agreements.

Bank loan in accounting

A loan taken from a bank or other financial institution is recorded on the liabilities side of the balance sheet, either as a long-term or short-term loan, depending on the repayment period. Most often, a bank loan is classified as a long-term liability.

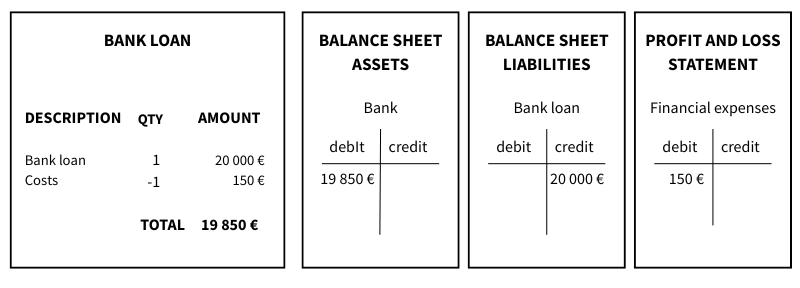

EXAMPLE

- Company takes out a bank loan of €20,000

- An initial fee of €150 is deducted from the loan amount

Loan withdrawal:

-

- DEBIT:

- (1910) Bank

- (9690) Financial expenses

- CREDIT

- e.g. (2361) Bank name and loan number

- DEBIT:

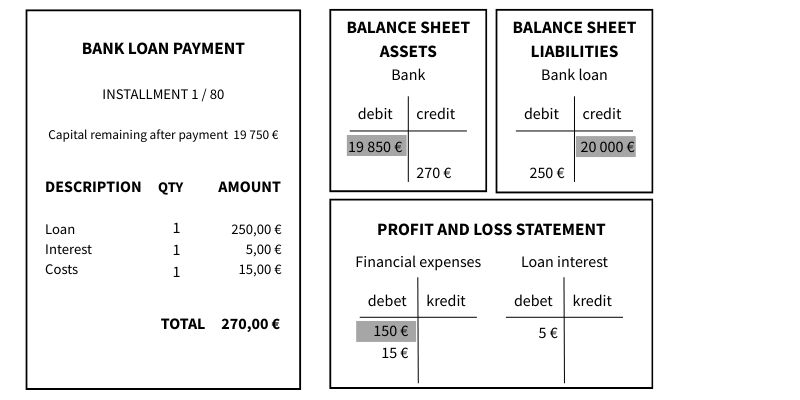

Loan repayment:

-

- DEBIT:

- (2361) Bank name and loan number

- (9690) Financial expenses

- (9460) Loan interest

- CREDIT

- (1910) Bank

- DEBIT:

💡 The loan decreased by 250 euros. When looking at the loan account, its balance is €19,750 (€20,000 – €250) , which corresponds to the remaining principal after the loan repayment.

Installment purchase in accounting

An installment purchase is a payment method where the price of a product or service is paid to the seller in pre-agreed installments. If the repayment period exceeds one year, the debt is classified as a long-term liability.

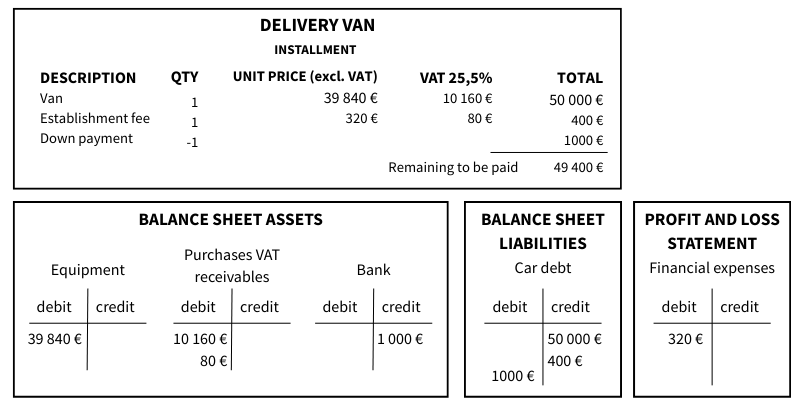

EXAMPLE

- A company buys a car for €50,000 through an installment plan.

- The car’s price and the installment setup costs include VAT.

- The company makes a €1,000 down payment from its bank account.

- A new account is created under the balance sheet’s liabilities for the installment debt – for example: (2682) Car model + registration number

Car and installment accounting entries:

-

- DEBIT:

- (1160) Equipment – The price of the car excluding VAT (€39,840) is recorded as a company asset.

- (1845) Purchases VAT receivables – The VAT on the car (€10,160) and the establishment fee (€80) are recorded as VAT receivables.

- (2682) Car installment debt – The €1,000 down payment is recorded here to reduce the total installment debt.

- (9690) Financial expenses – The establishment fee excluding VAT (€320) is recorded as a finance expense.

- CREDIT

- (2682) Car installment debt – The total purchase price of the car including VAT (€50,000) and the establishment fee including VAT (€400) are recorded here as the total installment debt.

- (1910) Bank account – The €1,000 down payment paid from the company’s bank account is recorded here.

- DEBIT:

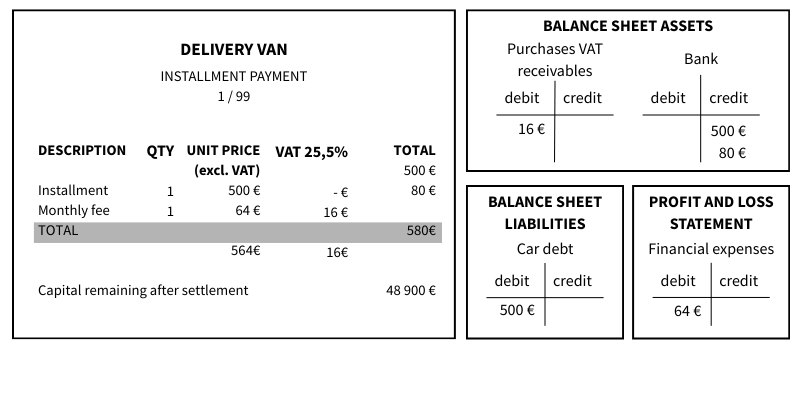

Installment payment reduction:

-

- DEBIT

- (1845) Purchases VAT receivables – The VAT portion of monthly fees (€16).

- (2682) Car installment debt – The installment portion (€500) is recorded here to reduce the remaining debt.

- (9690) Financial expenses – The price of the monthly fee excluding VAT (€64).

- CREDIT

- (1910) Bank account – The total installment payment (€580)

- DEBIT

It’s important to reconcile long-term loans regularly to ensure the liability account in the accounting records matches the actual remaining debt. Sometimes, an accountant might mistakenly record the entire installment payment as a reduction of the loan, even though part of it includes interest and fees. This error would cause the loan balance in the books to decrease faster than in reality, giving incorrect information. Regular reconciliation – even monthly – can save a lot of trouble at year-end.

Kokeile heti

Helppokäyttöinen ja edullinen SimplBooks kirjanpito-ohjelma. Ota käyttöön kahdessa minuutissa ja kokeile 30 päivää ilmaiseksi! Ohjelmalla on jo yli 20 000 tyytyväistä käyttäjää.

Leave a Reply