Depreciation of building in accounting (0)

Depreciation of a building in accounting follows the same principles as the depreciation of machinery or equipment. It can be done once a year during the preparation of financial statements, or, if preferred, on a monthly basis. In simple terms, depreciation is done by calculating the depreciation amount based on the building’s residual value and making the necessary accounting entry.

Depreciable vs. non-depreciable fixed assets

Fixed assets are assets acquired for use in a company’s operations and are not intended for resale. For tax purposes, fixed assets are divided into depreciable and non-depreciable categories.

As the name suggests, non-depreciable fixed assets do not lose value through use. Therefore, depreciation is generally not applied to non-depreciable assets. Instead, their acquisition cost (the value at which the asset was purchased) is deducted only when the asset is sold or otherwise disposed of. Typical examples of non-depreciable assets include land, shares, securities, and artworks.

Depreciable fixed assets, on the other hand, are used in the company’s operations and lose value over time. For tangible depreciable assets such as machinery and equipment, a maximum depreciation rate of 25% can be applied (or increased depreciation for the years 2020–2025). Building depreciation, however, follows its own rules.

Buildings in accounting

Depreciation of buildings differs from that of other assets, such as machinery or equipment, because building depreciation must be calculated separately for each individual building. In contrast, machinery and equipment can be depreciated collectively based on their total residual value.

If a company owns multiple buildings, it is practical to record them in the balance sheet so that they can be easily reviewed individually. This can be done by creating a separate account for each building or by grouping buildings with the same depreciation rate under a single account (e.g., “Buildings 4%”). If multiple buildings are recorded under one account, the depreciation for each building must still be tracked separately, for example, using an Excel spreadsheet.

Depreciation rates for buildings

Buildings and structures do not have a uniform depreciation rate; the applicable rate depends on the purpose of the building. The maximum annual depreciation rates are as follows:

- 7% of the undepreciated acquisition cost for:

- Retail buildings

- Warehouse buildings

- Factory buildings

- Workshop buildings

- Utility buildings

- Power plant buildings

- Or other comparable buildings

- 4% of the undepreciated acquisition cost for:

- Residental buildings

- Office buildings

- Or other comparable buildings

- 20% of the undepreciated acquisition cost for:

- Fuel tanks, acid tanks or similar metal or comparable storage structures

- Lightweight wooden or similar constructions

- Buildings or structures used exclusively for business-related research activities

It is important to note that the depreciation rate is determined by the building’s primary use. For example, if a company owns an industrial hall that is primarily used for industrial operations, a small office space in the corner does not affect the depreciation rate; the entire hall is depreciated at 7%. However, if the hall is used equally for both industrial and office purposes, depreciation can be split according to usage: 7% for the industrial portion and 4% for the office portion.

Recording building depreciation in accounting

Depreciation of buildings is recorded in the same way as the depreciation of other assets. In short, the building’s value is gradually transferred from the balance sheet to the income statement as an expense. thereby reducing the company’s taxable income.

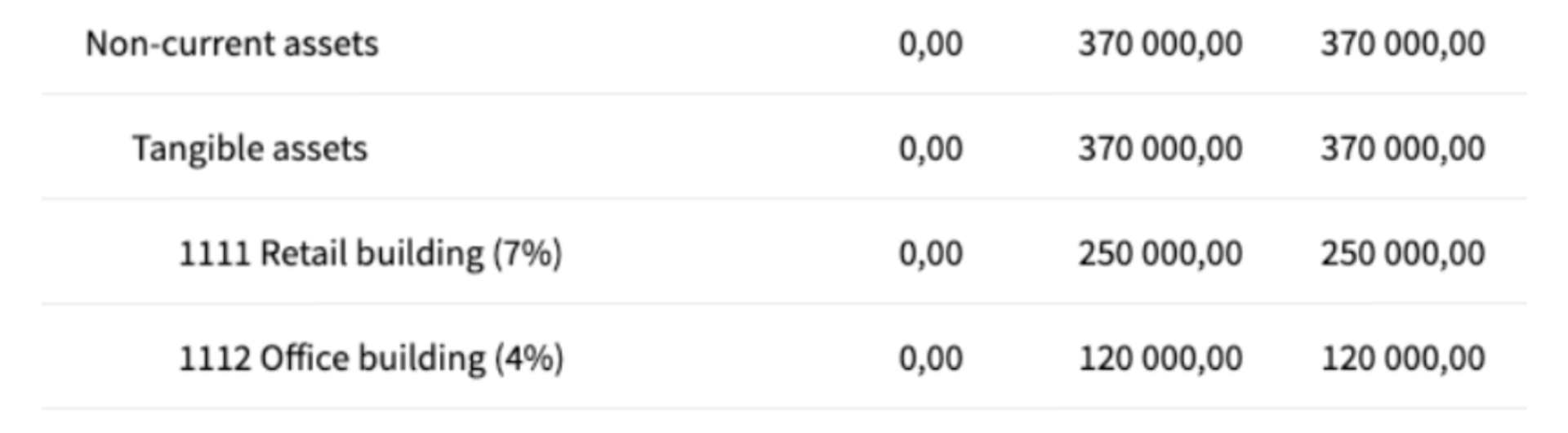

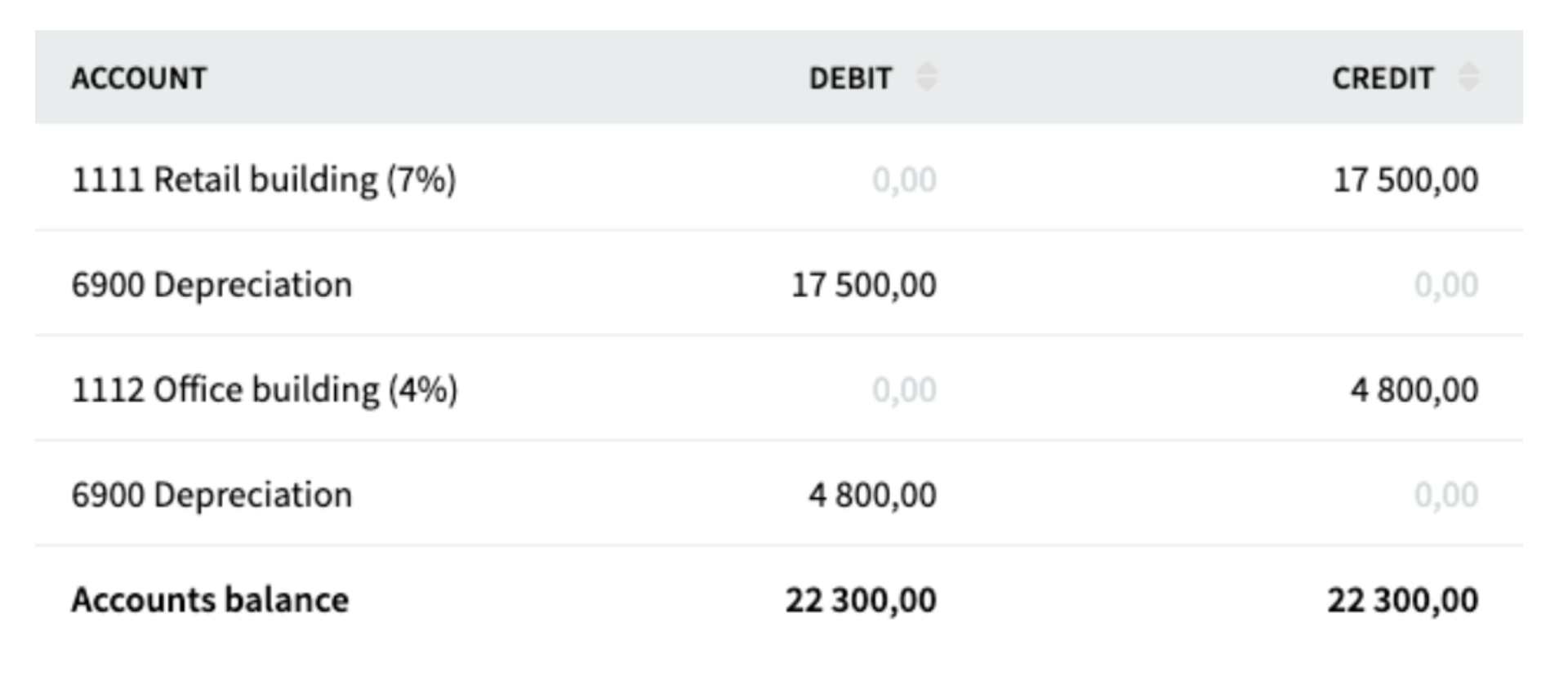

Retail Building

– Remaining undepreciated balance: €250,000

– Depreciation rate: 7%

– Depreciation amount (€250,000 × 7%): €17,500

Office Building

– Remaining undepreciated balance: €120 000

– Depreciation rate: 4%

– Depreciation amount (€120,000 × 4%): €4,800

Depreciation Entries:

– DEBIT: (6900) Income statement account “Depreciation”

– CREDIT: (1111 / 1112) Balance sheet accounts for buildings

Like machinery and equipment, the value of buildings decreases over time due to use and wear. Therefore, depreciation on buildings is recorded in the accounts to ensure that the wear-and-tear process is reflected in the company’s financial reports.

Try right away!

A more advanced and easy accounting software SimplBooks with over 10,000 active users - register an account and you can try 30 days free of charge and risk-free (no financial obligations shall arise). Or try our demo version!

Leave a Reply