What are accrued liabilities and accrued receivables? (0)

.Accrued liabilities and accrued receivables come into play when preparing or reversing financial statements. As the names suggest, these accounts are used to record income and expenses in connection with the financial statements. And they are reversed immediately after the new financial year begins – or later, once the payment transaction has taken place.

Accrued liabilities

Accrued liabilities include accrued expenses and deferred income. Accrued expenses refer to unpaid expenses and deferred income refers to income received in advance. In other words, if a company has unpaid expenses, they are recorded as liabilities. Or, if the company has already received money for the next fiscal year, the current fiscal year has a liability for the next fiscal year.

Accrued expense = An expense belonging to the current financial year that has not yet been paid as of the balance sheet date.

These are expenses that belong to the financial year but will be paid only in the following year. Usually, these are rental expenses or calculated expenses, such as unpaid interest, holiday pay and taxes.

EXAMPLE

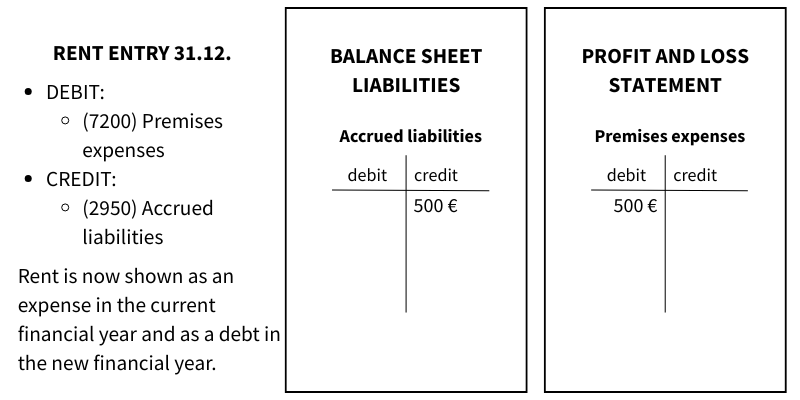

- Te company’s financial year ends on December 31st.

- The company has not paid the December rent as of 31.12.

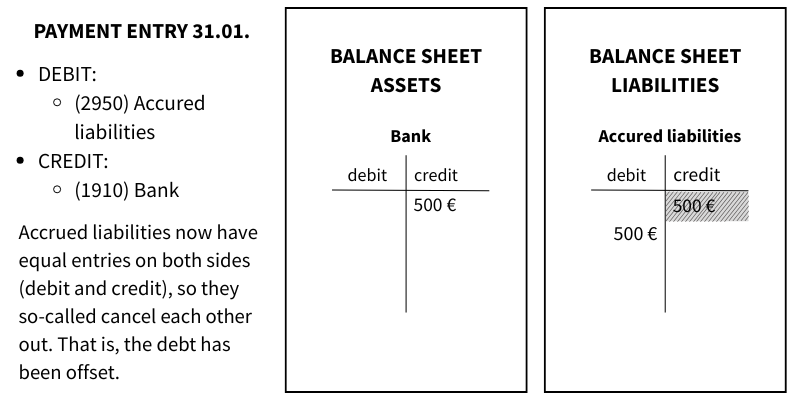

- The company pays the December rent on the last day of January.

Deferred income = Income belonging to the next financial year that has been received in advance.

These are funds received during the current financial year but belonging to the next financial year’s income. Examples include rent or interest received in advance.

EXAMPLE

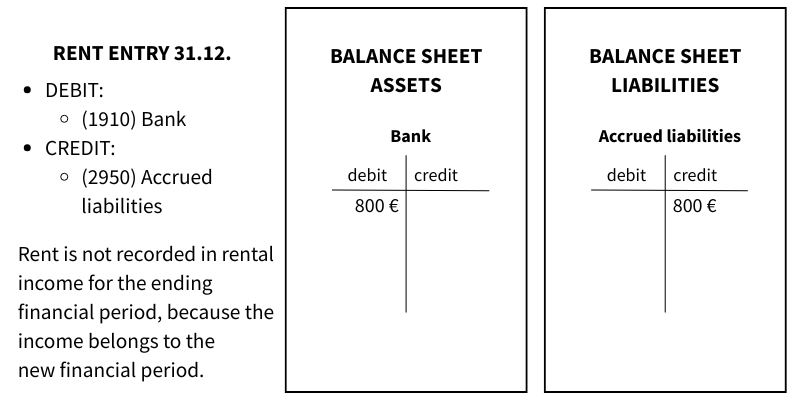

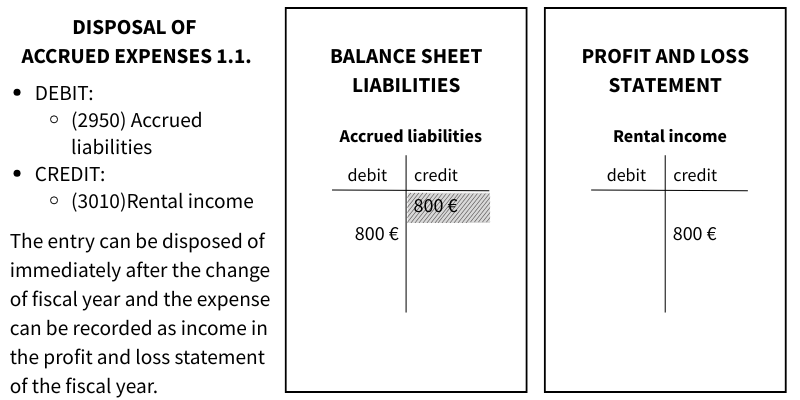

- The financial statements show that the accrued liabilities on the balance sheet include the amount received for January’s rent in the previous fiscal period, which is owed to the new fiscal period.

Accrued receivables

Accrued receivables include accrued income and prepaid expenses. Accrued income is income that has not yet been received, and prepaid expenses are expenses paid in advance. That is, if income belongs to the current financial year but will only be credited in the next financial year, the company is effectively receiving money from the next financial year. Or, if the company has paid expenses for the next financial year, it is again receiving money from the next financial year.

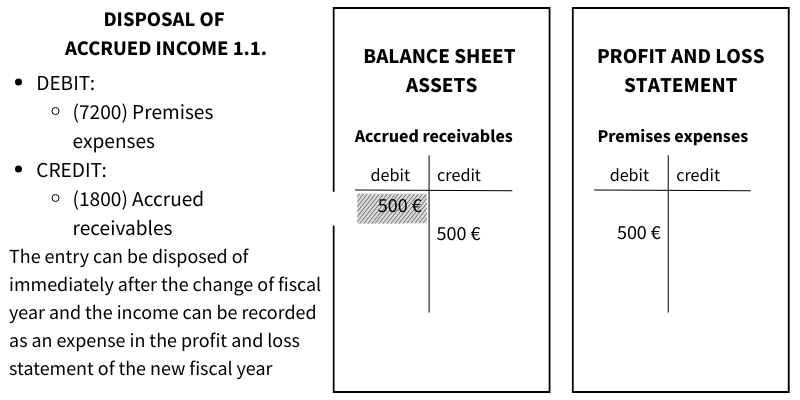

Prepaid expense = An expense paid in advance

Prepaid expenses are costs that belong to the next financial year but have already been paid in the current financial year. Prepaid expenses include, for example, insurance premiums or rent paid in advance.

EXAMPLE

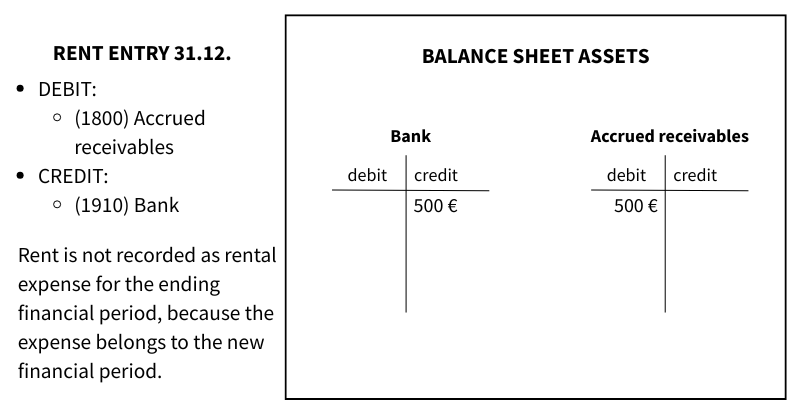

- The company’s fiscal year ends on December 31st.

- The company has paid January’s rent in December

- In the financial statements, the accrued receivables on the balance sheet show that the ending financial period has paid the rent for the new financial period. This can also be viewed as the new financial period owing the ending financial period the amount of January’s rent.

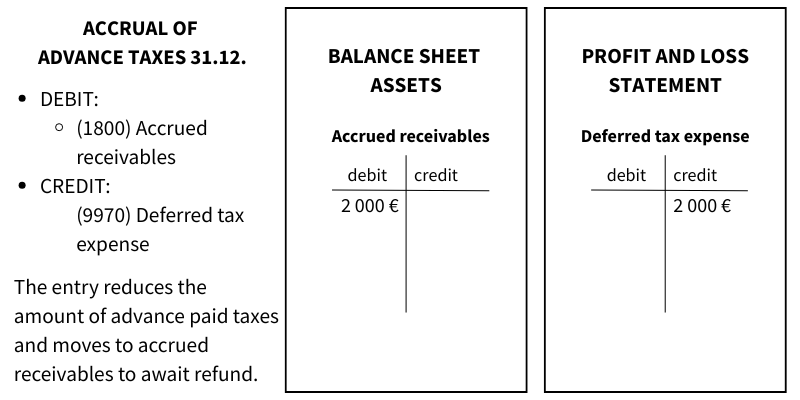

Accrued income = Income belonging to the current financial year for which payment has not yet been received by the balance sheet date.

Accrued income is income that belongs to the current financial year, but the money will not be received until the next financial year. Accrued income is income that is not based on an invoice and can include, for example, interest or overpaid advance taxes.

EXAMPLE

- The company’s financial year ends on December 31st.

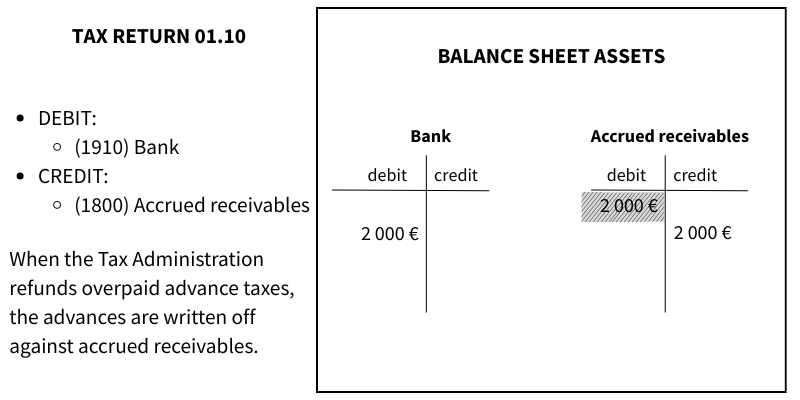

- The company has paid 2,000 euros too much in advance taxes. Tax Administration will refund them in the next financial year.

Accrued liabilities and accrued receivables should not be confused with accounts payable or accounts receivable. They are entirely different concepts. Accounts payable and receivable are always based on invoices, while accrued liabilities and receivables are more like calculated year-end adjustments. These items contain a lot of accounting jargon, but at the moment of preparing the financial statements, just ask yourself: “Is the closing financial year owed money or owing money to someone?”. The answer will tell you immediately which account you should use.

Try right away!

A more advanced and easy accounting software SimplBooks with over 10,000 active users - register an account and you can try 30 days free of charge and risk-free (no financial obligations shall arise). Or try our demo version!

Leave a Reply